Quick Read

-

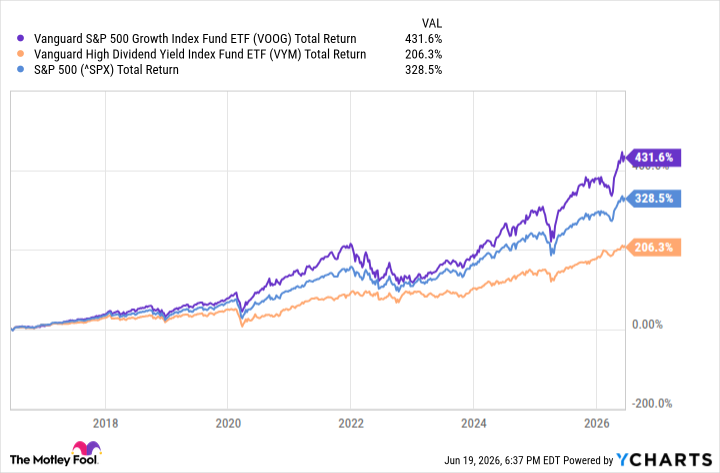

SPDR S&P 500 ETF Trust (SPY) has returned roughly 28% over the past year and 71% over five years despite multiple geopolitical shocks, demonstrating that investors who panic-sold missed substantial compounding gains. Goldman Sachs projects S&P 500 earnings around $310 versus the prior year’s roughly $270 range, with earnings—not headlines—driving long-term equity returns.

-

A retirement plan that withstands a 2% market move requires structural protection: cash reserves covering 1-3 years of spending, diversified allocation stress-tested against 25% drawdowns, and a written income plan mapping all withdrawal sources, ensuring emotional decisions don’t trigger permanent losses during temporary geopolitical or market disruptions.

-

The analyst who called NVIDIA in 2010 just named his top 10 stocks and SPDR S&P 500 ETF wasn’t one of them. Get them here FREE.

The host of Retire SMART Podcast Episode 405 offered a line that should sit on every pre-retiree’s refrigerator: “If the market moving 2% up or down in a single day makes you think you don’t have a good retirement plan, you don’t. I mean, that’s that simple.” The episode, titled Market Reactions Amidst Iran Conflict, framed it as a litmus test for whether your plan can absorb a geopolitical shock or whether you have been quietly riding a bull market and calling it strategy.

If a single rough headline pushes you to sell equities, move to cash, or rewrite your withdrawal strategy in a panic, you risk locking in losses, triggering avoidable taxes, and shortening the life of your portfolio by years. For a retiree drawing 4% annually, one emotional reallocation during a drawdown can permanently reset the income floor.

The analyst who called NVIDIA in 2010 just named his top 10 stocks and SPDR S&P 500 ETF wasn’t one of them. Get them here FREE.

The Verdict: The Host Is Right, and the Math Backs Him Up

A retirement plan that survives only when markets cooperate is just a mood dressed up as strategy. The financial concept underneath the quote is sequence-of-returns risk, the idea that the order of your returns matters enormously once you start withdrawing. Two retirees with identical average returns can end up with wildly different outcomes if one hits a 20% drawdown in year one and the other hits it in year fifteen.

Consider a 66-year-old with $1,000,000 split 60/40 between equities and bonds, withdrawing $40,000 a year. If equities drop 20% in year one and she sells stock to fund that withdrawal, she has converted a paper loss into a permanent one. The same drawdown in year fifteen, after years of compounding, barely registers. A real plan handles year-one risk by carving out 1 to 3 years of spending in cash and short-term bonds so the equity sleeve is never forced to sell into weakness.

The host’s point about market psychology supports this. “The market is forward thinking, 6 to 9 months ahead of the world economy. The market’s always looking forward.” On the Iran/oil situation specifically, he argued, “The market is saying, you know what, inflationary pressures are not gonna be real from this oil spike. They’re gonna come down and they’re gonna come down pretty quickly, probably over the summer.” Translation: by the time a retail investor reads the headline, the price already reflects the expected outcome.

The earnings backdrop matters here. The same segment cited Goldman Sachs (NYSE:GS) projecting S&P 500 earnings around $310 versus the prior year’s roughly $270 range. Earnings, more than headlines, drive long-term equity returns. The S&P 500, via the SPDR S&P 500 ETF Trust (NYSEARCA:SPY), is up about 28% over the past year and roughly 71% over five years, even after multiple geopolitical scares. Investors who exited on each scary headline forfeited that compounding.

Who the Advice Fits, and Who Should Worry

This advice fits retirees and pre-retirees aged 55 to 75 with a written income plan, a diversified allocation, and at least 12 to 24 months of cash-equivalent reserves. For them, a 2% day is noise.

It does not fit a 62-year-old with $400,000 entirely in S&P 500 index funds, no bond allocation, no cash bucket, and a plan to retire next year on portfolio withdrawals alone. That investor is not diversified, has no drawdown buffer, and is one bad year away from a forced reset of lifestyle. For that profile, panic on a 2% day is rational, because the plan genuinely cannot absorb a 20% one.

What to Actually Do This Week

The host’s behavioral guidance is the practical core: “Don’t pay attention to all the noise. Work with a competent professional who has a diversified allocation set up for you to weather the storm, good or bad, and that you have a retirement and income plan set up so that you don’t have to worry about the news.” Translate that into specific homework:

-

Stress-test your allocation. Pull up your portfolio and apply a hypothetical 25% equity drawdown. If the resulting balance cannot fund 20-plus years of your needed withdrawals, your equity sleeve is too large or your spending too high.

-

Build the cash bucket. Aim for 1 to 3 years of withdrawals in money market funds, Treasury bills, or short-duration bond funds. This buffer lets you ignore a 2% day.

-

Write the income plan. Map every dollar of expected retirement spending to a source: Social Security, pension, bond interest, dividends, systematic withdrawals. Gaps are where panic lives.

-

Define your drawdown tolerance in dollar terms. “I can handle 20%” sounds fine until 20% of $1.2 million is $240,000. Know the dollar number before the market shows it to you.

A plan built for stress treats a 2% day as weather. If yours treats it as a crisis, the fix is structural.

The analyst who called NVIDIA in 2010 just named his top 10 AI stocks

This analyst’s 2025 picks are up 106% on average. He just named his top 10 stocks to buy in 2026. Get them here FREE.